1. What is the Asia-Pacific Smart Mining Market overview – definition, scope, and significance?

The Asia-Pacific Smart Mining Market encompasses technology‑driven solutions that enhance safety, efficiency, and productivity in mining operations across the region. It includes hardware such as sensors, autonomous equipment, and communication devices; software and solutions for data analytics, fleet management, and predictive maintenance; and services that integrate these components into underground and surface mining activities. The market’s significance lies in its ability to address labor shortages, stringent environmental regulations, and the demand for higher ore recovery rates, positioning the Asia‑Pacific region as a leader in the digital transformation of mining.

2. What are the key drivers, restraints, challenges, and opportunities shaping the Asia-Pacific Smart Mining Market?

Key drivers include rapid urbanization, rising demand for minerals, and governmental support for Industry 4.0 adoption. The need to improve worker safety and reduce operational costs further propels investment in smart technologies. Restraints stem from high upfront capital requirements and limited skilled personnel to manage complex systems. Challenges involve integration with legacy equipment and data security concerns. Opportunities arise from expanding autonomous vehicle fleets, AI‑enabled predictive analytics, and partnerships between technology firms and traditional mining companies to co‑develop customized solutions.

3. Which growth trends are currently influencing the Asia-Pacific Smart Mining Market?

Current trends feature the shift toward fully autonomous drilling rigs, the proliferation of IoT‑based monitoring networks, and the use of cloud platforms for real‑time data visualization. Edge computing is gaining traction to reduce latency in underground environments, while blockchain pilots are being explored for transparent supply‑chain tracking. Additionally, an increasing number of mining sites are adopting integrated hardware‑software ecosystems that support remote operations and workforce training through virtual reality.

4. How did COVID‑19 impact the Asia-Pacific Smart Mining Market and what is the recovery trajectory?

The pandemic caused temporary shutdowns of several mining projects, leading to delayed capital expenditures on smart technologies. However, the crisis highlighted the value of remote monitoring and automation, accelerating interest in contact‑free solutions. Post‑2021, the market rebounded as operators prioritized resilience, resulting in a faster than expected uptake of cloud‑based analytics and autonomous equipment. The recovery trajectory remains positive, supported by renewed government stimulus for digital infrastructure.

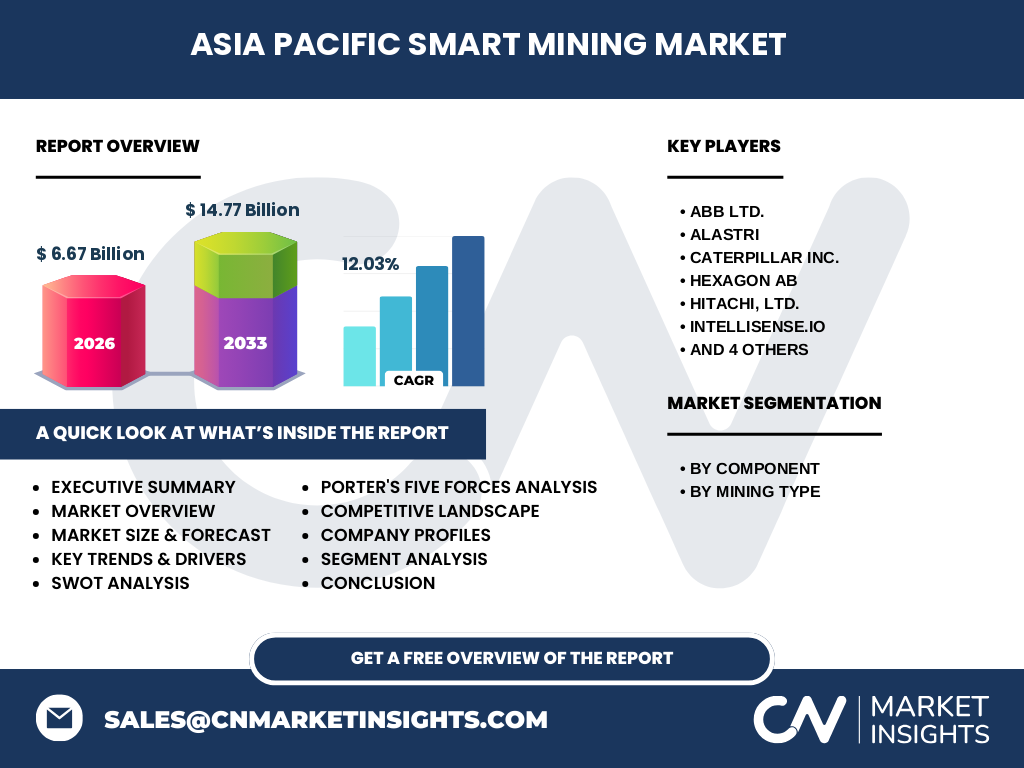

5. Who are the major competitors in the Asia-Pacific Smart Mining Market and what is the level of market consolidation?

Key competitors include ABB Ltd., Caterpillar Inc., Hexagon AB, Hitachi, Ltd., Rockwell Automation, Inc., SAP SE, Trimble Inc., alongside emerging specialists such as Alastri, Intellisense.io, and MineSense. The competitive landscape shows moderate consolidation, with large multinationals acquiring niche technology firms to broaden their solution portfolios. Strategic alliances are common, enabling players to combine hardware expertise with advanced software capabilities.

6. What are the high‑level findings presented in the executive summary?

The executive summary underscores a robust market valued at USD 6.67 billion in 2026, with a projected increase to USD 14.77 billion by 2033, reflecting a CAGR of 12.03 %. Growth is driven by digital‑first mining strategies, strong governmental policies, and rising demand for critical minerals. hardware remains the largest component segment, while software and services exhibit the fastest growth rates. Underground mining adoption leads in technology uptake, followed by surface operations. The report highlights strong investment potential, especially in AI‑enabled analytics and autonomous fleets.

7. What forecasts are provided for the Asia-Pacific Smart Mining Market from 2025 to 2032?

Based on the stated CAGR of 12.03 %, the market is expected to maintain a steady upward trajectory, expanding from its 2026 baseline of USD 6.67 billion to well beyond USD 14.77 billion by the end of the forecast horizon. The growth is anticipated across all segments, with software and solution revenues outpacing hardware due to recurring licensing models, while services will grow in line with increasing system integration projects.

8. How is the market sized and shared by component and mining type segmentation?

Segmentation by component divides the market into hardware, software and solution, and services. Hardware accounts for the majority of the current market spend, reflecting purchases of sensors, autonomous vehicles, and communication infrastructure. Software and solution, encompassing data platforms and analytics tools, is the fastest‑growing sub‑segment, driven by demand for predictive maintenance and fleet optimization. Services—covering system integration, consulting, and after‑sales support—represent a smaller yet increasingly important share as operators seek end‑to‑end implementation.

By mining type, the market separates into underground and surface mining. Underground mining leads in smart technology adoption because of the heightened safety requirements and the complexity of underground environments, which benefit most from real‑time monitoring and autonomous equipment. Surface mining follows, focusing on fleet management and ore‑grade optimization.

9. What is the geographic distribution of the Asia-Pacific Smart Mining Market?

Geographically, the market is concentrated in major mineral‑rich economies such as China, Australia, and Indonesia. China’s extensive coal and rare‑earth production drives substantial hardware deployment, while Australia’s large iron‑ore and copper sectors fuel software and services adoption for large‑scale fleet management. Southeast Asian nations are emerging as growth hotspots, supported by new mining concessions and government incentives for technology upgrades.

10. Can you provide a detailed regional performance analysis?

In China, the market benefits from strong state‑led digital initiatives, resulting in accelerated deployment of IoT sensors and AI analytics in both underground and surface mines. Australia demonstrates high per‑mine spending on autonomous haul trucks and cloud‑based fleet coordination, supported by robust mining financing ecosystems. Indonesia shows rapid growth in surface mining automation, driven by government policies encouraging mineral export value addition. Overall, the region exhibits varied maturity levels, with developed economies leading in advanced autonomy and emerging markets focusing on incremental digitization.

11. Which companies lead the Asia-Pacific Smart Mining Market and what are their strategic approaches?

ABB Ltd. leverages its expertise in electrification and robotics to provide integrated automation platforms. Caterpillar Inc. focuses on autonomous haulage systems and data‑driven equipment management. Hexagon AB supplies advanced surveying and 3D‑mapping solutions that feed into mine planning software. Hitachi, Ltd. emphasizes AI‑enabled predictive maintenance. Intellisense.io and MineSense specialize in sensor‑based ore‑grade monitoring, offering niche differentiation. Trimble Inc. combines positioning technology with cloud analytics to support fleet optimization. These leaders pursue a mix of organic R&D, strategic acquisitions, and joint ventures to broaden their portfolios.

12. What does Porter’s Five Forces analysis reveal about the market?

Supplier Power: Moderate, as component manufacturers (sensor, semiconductor) are fragmented, allowing buyers to negotiate. Buyer Power: Growing, because large mining corporations consolidate purchasing and demand integrated solutions. Threat of New Entrants: Low to moderate; high capital requirements and technology expertise create barriers, though startups can enter via niche sensor or AI services. Threat of Substitutes: Limited, since traditional manual processes cannot match the efficiency gains of smart systems. Competitive Rivalry: High, driven by aggressive product roll‑outs, strategic alliances, and continuous innovation.

13. What are the SWOT insights for the Asia-Pacific Smart Mining Market?

Strengths: Strong demand for safety and efficiency, supportive regulatory frameworks, and presence of global technology leaders. Weaknesses: High implementation costs and skills gap in advanced analytics. Opportunities: Expansion of autonomous fleets, growth of AI‑driven predictive maintenance, and increasing investment in renewable‑powered mining operations. Threats: Cybersecurity risks, fluctuating commodity prices affecting capital spending, and potential regulatory changes regarding autonomous equipment.

14. How is the value chain structured for smart mining in Asia‑Pacific?

The value chain begins with raw material extraction, followed by sensor and hardware installation (e.g., LiDAR, vibration monitors). Data acquisition moves to edge devices, which transmit information to cloud or on‑premise platforms. Software providers apply analytics, machine learning, and visualization tools to generate actionable insights. Integration services customize solutions for specific mine sites, while after‑sales support maintains system performance. Finally, end‑users—mine operators—leverage the insights to optimize production, safety, and maintenance schedules.

15. What key investment insights should stakeholders consider?

Investors should focus on companies that offer end‑to‑end solutions, combining hardware, software, and services, as these capture recurring revenue streams. Startups with proprietary sensor technologies or AI algorithms present high‑growth potential, especially when partnered with established equipment manufacturers. Geographic diversification toward Australia and Indonesia can balance risk, while monitoring policy developments in China will identify early‑stage funding opportunities. Overall, the projected 12 % CAGR signals an attractive long‑term investment horizon.

16. What are the main conclusions drawn from the market study?

The Asia‑Pacific Smart Mining Market is on a decisive growth path, driven by digitalization imperatives, safety concerns, and the pursuit of operational excellence. Hardware remains the backbone, yet software and services are set to outpace it in revenue growth. Regional dynamics show mature adoption in China and Australia, with emerging upside in Southeast Asia. Competitive pressures are intensifying, encouraging innovation and collaboration among the key players listed.

17. Which research methodology was employed to compile this report?

The study combined primary interviews with industry executives, technology providers, and mine operators, alongside secondary data from company filings, government publications, and reputable market databases. Trend analysis, regression modeling, and CAGR calculation were applied to forecast market size through 2033. Segment validation was performed through cross‑checking of component and mining‑type data against publicly disclosed project awards.

18. What is the scope of this research and its limitations?

The research covers the Asia‑Pacific region, focusing on smart mining hardware, software and solutions, and related services for underground and surface mining operations. It includes market size, segmentation, competitive landscape, and forward‑looking forecasts up to 2033. Limitations arise from the reliance on publicly available financial disclosures and the exclusion of confidential contract values, which may affect granular market‑share precision.

19. Which key companies have announced recent developments in the Asia‑Pacific Smart Mining Market?

ABB Ltd. recently launched a cloud‑based digital twin platform for underground mines in Australia. Caterpillar Inc. announced the rollout of its new autonomous haulage system at a major Indonesian copper mine. Hexagon AB introduced an AI‑enhanced 3D‑mapping solution for Chinese coal operations. Hitachi, Ltd. unveiled a predictive maintenance suite integrating edge sensors with SAP SE’s analytics cloud. Intellisense.io secured a partnership with a leading Australian mining consortium to trial real‑time ore‑grade sensors. MineSense released an upgraded sensor suite for surface mining applications in Indonesia. Rockwell Automation, Inc. formed a joint venture with a regional equipment integrator to deliver end‑to‑end automation services. Trimble Inc. expanded its fleet‑management SaaS offering across several Chinese surface mines.